Accounting for refrigerants: Toward a sustainable business

If you want to conduct a greenhouse gas (GHG) inventory to address the emissions associated with your company’s activities, you may want to start by reviewing the GHG Protocol Corporate Standard, the authoritative source on methodologies for accounting and reporting on GHG emissions. As you work through the list of required gases to report on, you may be shocked to find two classes of high-GWP and ozone-depleting refrigerant gases, CFCs and HCFCs, omitted from this list.

Why are CFCs and HCFCs not included in the Greenhouse Gas Protocol?

National reporting guidelines for GHG emissions inventories are established by the United Nations

Framework Convention on Climate Change (UNFCCC) and the Kyoto Protocol. The GHG Protocol mirrors these criteria for its accounting and reporting framework to align with national inventory practice. As scientific developments are made, the UNFCCC/Kyoto Protocol adjusts international accounting and reporting rules, which the GHG Protocol reflects in its own guidance.

Leading reporting guidance commonly excludes CFCs, HFCs, and halons from its inventory requirements due to the regulation and phase out of these substances by the Clean Air Act and The Montreal Protocol on Substances that Deplete the Ozone Layer.

Studies indicate that large banks of halocarbons continue to leak from old equipment even after production of these chemicals has terminated, and will potentially contribute emissions equivalent to more than 21 billion metric tons of CO2 if left unaddressed.

Creating a Comprehensive GHG Inventory

Given the gravity of this potential impact, CFC and HCFC emissions should be included in your corporate inventory. Beyond the GHGs covered by the UNFCCC/Kyoto Protocol, the GHG Protocol encourages reporting emissions data from other GHGs, including CFCs and HCFCs. While emissions of these gases may be reported outside the scope of a corporate inventory, this level of disclosure serves to bolster transparency by communicating your organization’s commitment to climate mitigation through targeted, specific action.

To account for these emissions:

- Gather your service records, and identify the total mass (in pounds) of each type of refrigerant added to equipment throughout the year. (It may be that the records indicate you have been recharging a leaking system with the amount of material added to equipment equal to the amount of refrigerant that actually leaked.)

- Convert the volume of each refrigerant type added to systems throughout the year into metric tons.

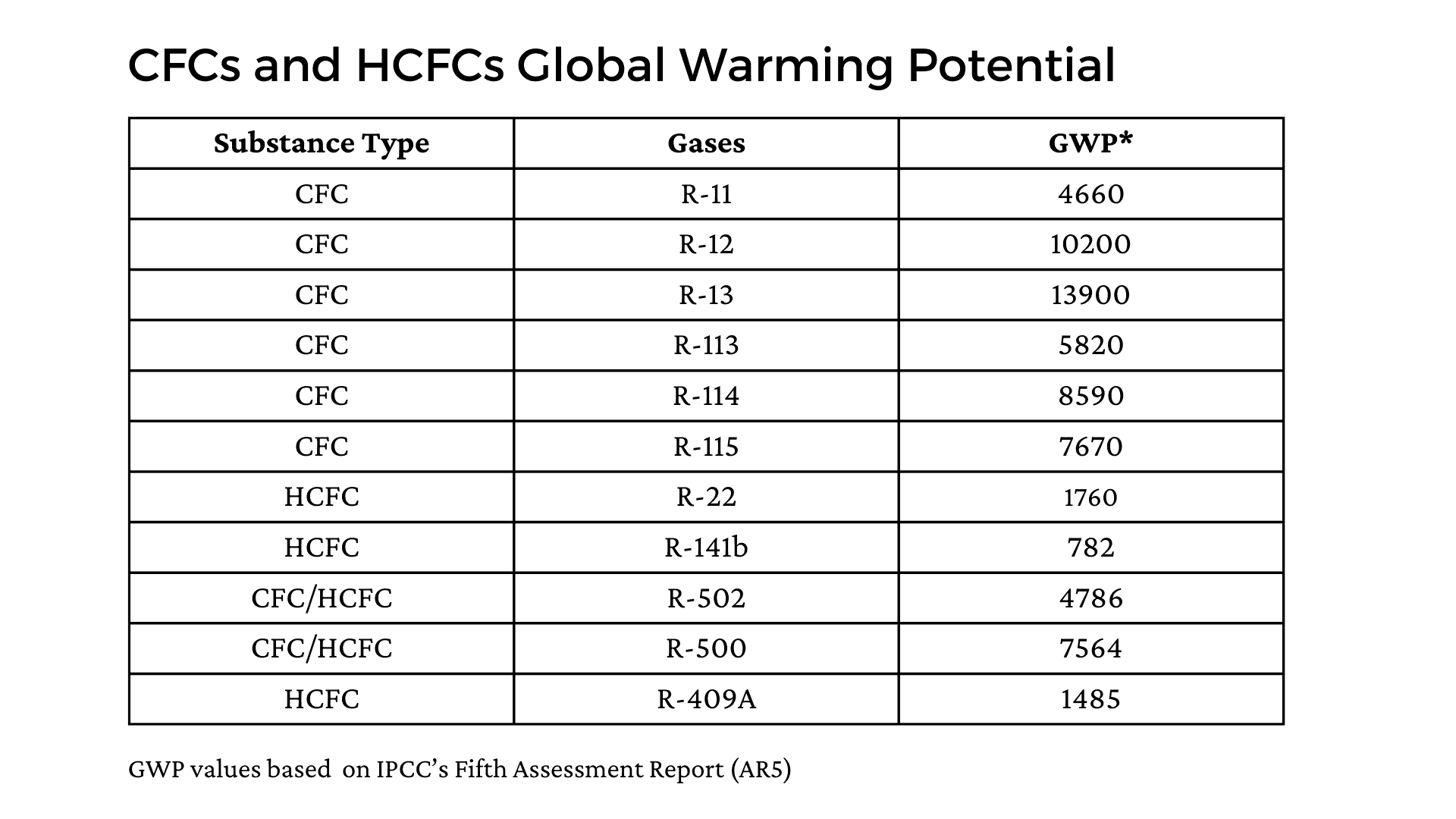

- Multiply the volume of each refrigerant type by its global warming potential (GWP) to determine the total amount of potential emissions in terms of carbon dioxide equivalent. CFC and HCFC emissions should be reported as a separate line item to distinguish them from Scope 1, 2, or 3 emissions.

It is also helpful to compile a basic refrigerant inventory for your building or portfolio. Having this information in one place will quantify the emissions risk of your refrigerants, and can help to incorporate environmental considerations when making retrofit or replacement decisions. To do so:

- Determine the full charge of systems and stockpiles of refrigerant by reviewing systems information plates, and equipment and purchasing records. This total can tell you your total volume of refrigerant (list by refrigerant type).

- Convert the volume to metric tons.

- Multiply the volume of each refrigerant type by its global warming potential (GWP) to determine the total amount of potential emissions in terms of carbon dioxide equivalent.

“Safe” Boundaries and the SBTi

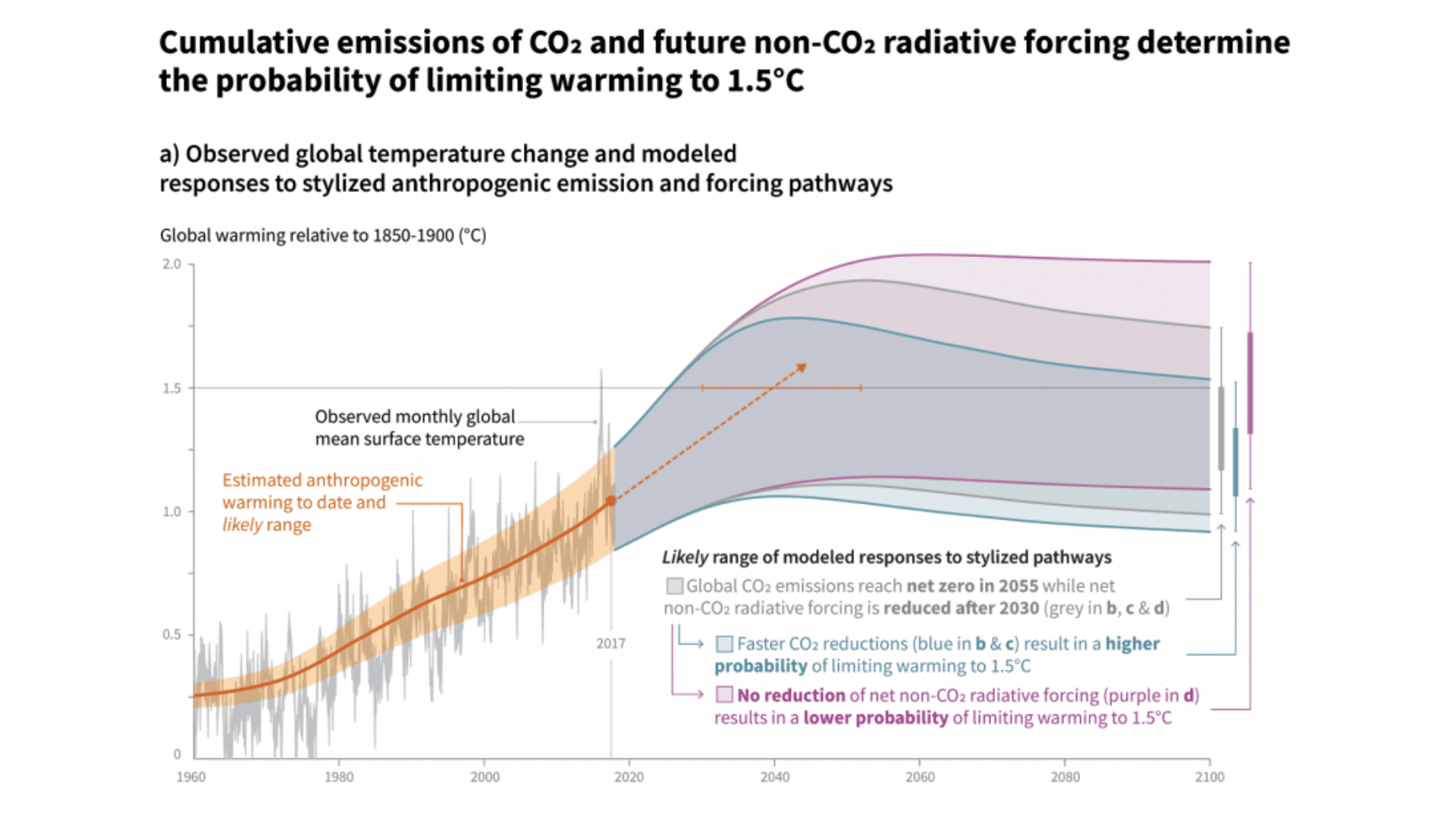

A 1.5 ℃ difference in temperature might offer some respite during the brutal winter, allowing you to wear a light jacket in lieu of your usual heavy-duty parkas. But against the backdrop of impending climate catastrophe, global temperature stabilization within the “safe boundary” (less than 1.5 ℃) is critical. Analysis conducted by the Earth Commission indicates that global mean surface temperatures must remain at or below 1.5 ℃ to limit the exposure of global communities to unprecedented temperatures and long-term sea level rise. Even at this level, it is still expected to impact hundreds of millions of people. Despite the urgency of this crisis, global policies currently in effect are still projected to allow for a 2.7°C rise in temperature by 2040.

For this reason, the Science-Based Target initiative (SBTi), a partnership between the Carbon Disclosure Project, the United Nations Global Compact, World Resources Institute, and the World Wide Fund for Nature was formed, with the goal of helping companies mobilize toward sustainable practices. While providing technical assistance and expert advice, they call on companies to invest in climate change mitigation activities outside their value chain that contribute to societal net-zero goals, referred to as Beyond Value Chain Mitigation (BVCM).

Companies can do their part by financing projects that reduce emissions, but this type of direct action also needs to increase by at least seven times by 2030, reaching a cost of at least USD 4.3 trillion per year, compared to approximately USD 665 billion today. While private sector climate finance is increasing, the Climate Policy Institute argues that it is not doing so at the necessary pace considering public sector capacity constraints.

Source: IPCC, Special Report: Global Warming of 1.5℃. Summary for Policymakers.

Source: IPCC, Special Report: Global Warming of 1.5℃. Summary for Policymakers.

Offsets: Immediate Actions

Offset projects are a class of BVCM strategies under the SBTi protocol that, with proper design and implementation, can contribute significantly to corporate sustainability goals.

Carbon offsets are emissions reduction activities used to compensate for emissions that occur elsewhere. The benefits accrued from offset projects are realized as carbon offset credits; one offset credit represents an emissions reduction of one metric ton of CO2 or an equivalent GHG amount (mtCO2e). These transferable units are delivered by independent certification institutions or governmental bodies. As a purchaser of a credit, you leverage the opportunity to advance your sustainability goals by “retiring” the credit to claim the associated benefits.

Carbon offsets can be an effective mitigation strategy for both reducing and communicating the gravity of your climate impact and associated efforts. When purchasing offsets, be sure to choose high-quality projects that are: additional (emissions reductions would not occur without revenue from the sale of carbon credits), permanent, and accurate (not overestimated).